RPM greenfield market report

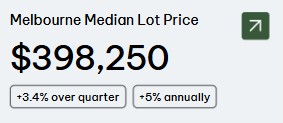

In Victoria to buy a house you need roughly 45% of average income to service a mortgage where as in Sydney you need 68%.

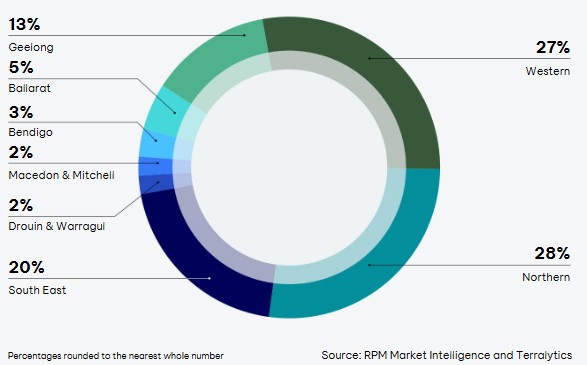

WESTERN GROWTH CORRIDOR = 937 lot sales in Q1 2026 down 40% from Q4 2025

NORTHERN GROWTH CORRIDOR = 981 lot sales in Q1 2026 down 29% from Q4 2025

SOUTH EAST GROWTH CORRIDOR = 688 lot sales in Q1 2026 down 31% from Q4 2025

GREATER GEELONG = 471 lot sales in Q1 2026 down 10% from Q4 2025

BALLARAT = 174 lot sales in Q1 2026 down 28% from Q4 2025

BENDIGO = 100 lot sales in Q1 2026 down 30% from Q4 2025

MACEDON & MITCHELL = 78 lot sales in Q1 2026 down 5% from Q4 2025

DROUIN & WARRAGUL = 86 lot sales in Q1 2026 down 21% from Q4 2025

These pullbacks are being put down to the two consecutive RBA rate hikes in February and March and broader deterioration of household consumer confidence.

Oliver Hume Market report Q1 2026

What greenfield projects need to succeed.

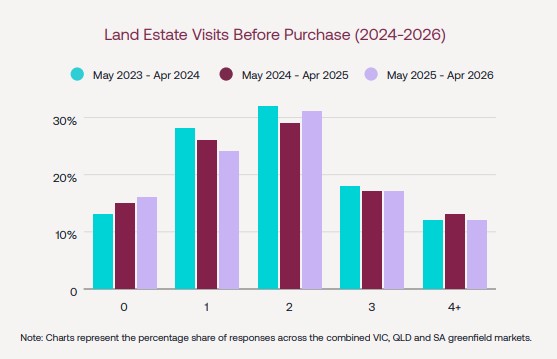

Greenfield markets are under increasing pressure to ‘standout’ and respond to consumer needs. Location, affordability, lot size/availability remain the top purchasing drivers. More than 80% of purchasers have “average to strong” knowledge of the area, while around 70% have two or fewer estate visits. Purchasers aged 33–55 accounted for ~80% of buyers, while First Home Buyers remained the largest buyer cohort at ~40%.

With buyers having fewer estate visits and relying more on digital and referral channels, projects will need to communicate product suitability more efficiently through interactive digital tools.

$47 billion housing system rebuild

- Building the homes Australia needs so housing becomes more affordable

- Levelling the playing field for first home buyers so more Australians can own a home of their own

- Making renting fairer and more affordable so renters can live in security and plan for the future

- Growing the social and affordable housing sector so more Australians have a stable place to call home

- Closing the housing gap in genuine partnership with First Nations Australians

- Supporting people experiencing homelessness, crisis, and family and domestic violence with a strengthened system

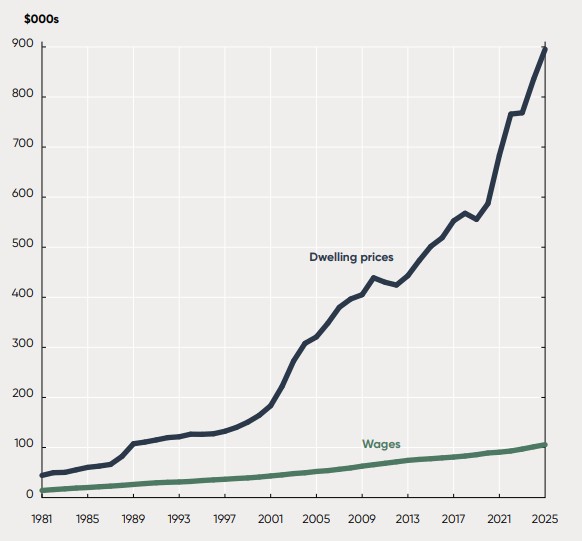

Earnings and dwelling prices since 1981

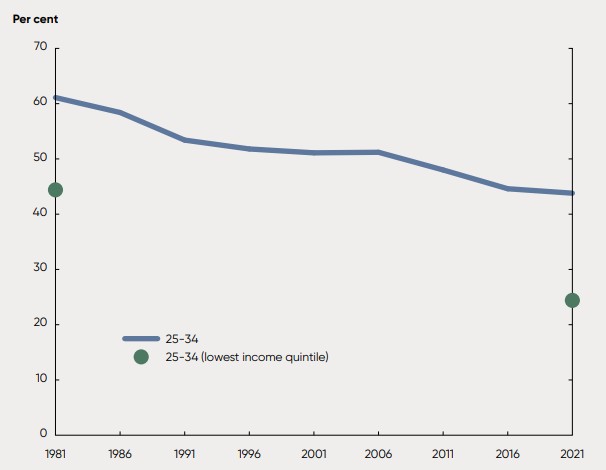

Home ownership rates for households aged 25-34